Bravo Brio Restaurant Group (BBRG) owns and

operates two Italian restaurant brands, BRAVO! Cucina Italiana (BRAVO!) and

BRIO Tuscan Grille (BRIO).

Casual dining continues to be a difficult

industry for investors. It’s rising wage costs, food inflation and simply too many

restaurants. Financially, Bravo gross and operating margins continue to decline

impacted by wages, food inflation and slightly lower average check size. Further, long term debt

was 184.906M for year ending 2009. Still significant but LTD reduced to the MRQ 122.189M.

My investment interest in BBRG; relative

valuation, mean reversion opportunity and its capital allocation priorities

that focus on shareholder value with opportunistically

share repurchases, and reducing debt.

BRIO moved higher to $4.88 or 8% over the last 2 days. It’s

still bouncing near its 52 week low price of $4.50.

Mid day 09/07/16 BBRG is up another ~2%.

But even with the 10% 3 day move, I will continue to finish the post. Hopefully

for current shareholders management is buying back shares or paying down debt with their positive operating cash flow. The lower stock price may be the signal

to management; focus capital allocation on a more aggressive share buyback.

Market capitalization 72.48M, Enterprise

value 113.48M, EV/Revenue .27, EV/EBITDA 3.62, CFFO TTM per share $2.27, FCF TTM

per share $1.12, 52 week change -60%, 52 week low $4.50, 52 week high = 12.74, insider

ownership 9%

Table below shows the valuation changes from Q1 2015 to current.

Table below shows the valuation changes from Dec 2011 to current.

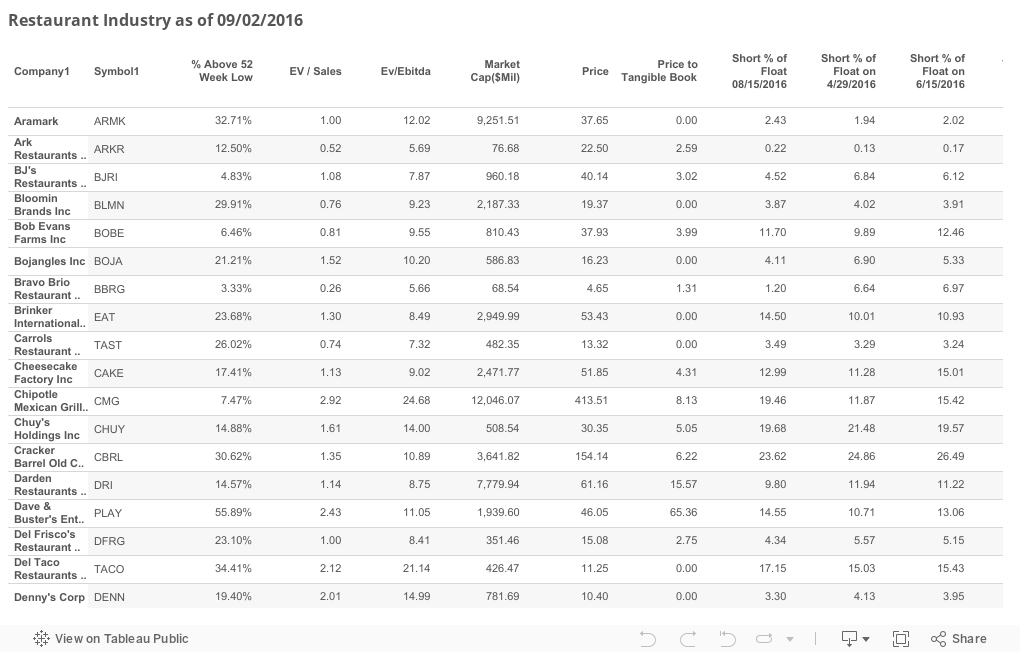

Table immediately below shows RESTAURANT industry valuation. Note the large drop in shorts % Float for BBRG. BBRG short % float 6.97% on 6/15/16 to current 08/15/16 1.20%