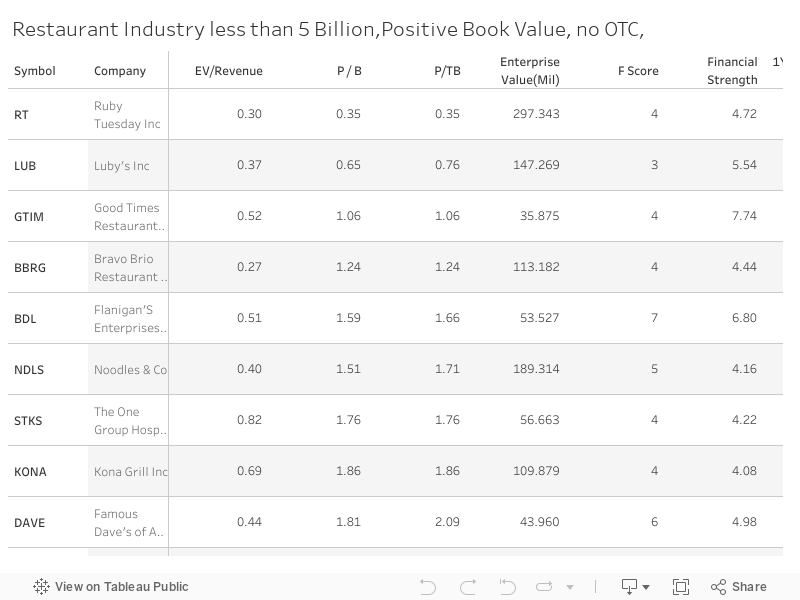

Luby’s, Inc. (LUB) operates and franchises restaurants and contract food services. Their brands include Luby's Cafeteria, Fuddruckers, Luby's Culinary Contract Services and Cheeseburger in Paradise.

Founded in 1947 with 7,988 employees and headquartered in Houston, Texas. As of December 21, 2016; 173 owned and operated restaurants, 91 traditional cafeterias, 73 gourmet hamburger restaurants, eight casual dining restaurants and one primarily seafood. Further, 23 Culinary Contract Services locations,48 franchisees operating 113 Fuddruckers restaurants.

Investment Thesis Summary:

Mean reverting unreasonably cheap valuation (historical and industry relative discounted valuation.

Skin in the game with management's material 33% Insider Ownership. Founders/Family C. Pappas owns 14.6%,H. Pappas 13.28%. Outside institutional ownership with long time holder Hodges Capital at 15.87% of the float or 10.20% shares outstanding.

Margin of Safety supported by meaningful Real Estate Ownership below fair market value. Real Estate Ownership; 69 Luby's, 22 Fudruckers, Non-operating properties with a carrying value of $7.1 million listed on recent balance sheet as held for sale for discontinued operations. In addition, one owned property with a carrying value of approximately $1.9 million and one owned other-use property which is used as a bake shop supporting restaurants.Think of the future impact of these rent free locations or sale lease back.

Significant insider buying over the prior two years. 802,549 shares purchased during 2015 for $4.99 per share or $2,699,257.During 2016 73,777 shares purchased for $4.63 per share or $342,001. Indirect buys for 2017 were 19,587 shares for $4.25 per share.

Mean reverting price performance, 60% off 5 year high and a -20% 52 week return.

Clean Capital structure with stable share count from 2010. Non current liabilities were reduced from 50.44M fiscal year ending 2014 to 44.48M or 12% reduction to the most recent quarter.Sale of balance sheet listed properties will further benefit.

Valuation:

Market Cap:104.55M , Enterprise Value:139.31M: Price is $3.61 near 10 year low.

Price/Tangible Book (mrq) = 0.63 versus an average P/TB value of 1.12 from 2010 to 2013. Industry Median P/TB is 2.91 versus .63 for LUB or its historical low of .56

EV/Revenue = .33 versus and average EV/Revenue of .55 from 2010 to 2013. Industry Median P/S= 1.05 vs LUB: 0.27

EV/EBITDA = 9.52 ,Revenue(ttm)396.3

EBITDA as measured in their bank covenants is 17.50M on trailing 4 quarter basis, 18.20M removing under-performing closed stores.

Revenue Per Share (ttm) 13.54 versus an average revenue per share of 11.67 from 2010 to 2013. Industry Median P/S is 1.05 vs LUB's P/S of 0.27

Quarterly Revenue Growth (yoy)-5.20% ,EBITDA (TTM) 14.63M

Gross Profit (ttm)256.45M versus a MC of only 104.54M and EV 139.39M

EV/Gross Profit = 2.54 versus and average EV/Gross Profit of 3.26 from 2010 to 2013

Operating Cash Flow (ttm) 10.76M ,52-Week Change -19.77%

52 Week High:$5.10,52 Week Low: $3.45

Shares Outstanding 28.96M , Float 17.34M (note small float balance making a going private transaction a possibility and beneficial to owners at the current valuation)

% Held by Insider: 33.51% , % Held by Institutions: 38.70%

Short % of Float: 1.20% (shorts declining over the past 6 months)

Negatives: CEO C Pappas age 70 owns 14.60% and executive director H Pappas age 72 owns 13.28% are apparently satisfied with their salary and time to run other investments. Additionally, unfriendly shareholder ownership evidenced by not one analyst on the most recent earnings call.

Conclusion: Great valuation metrics based on sales, EBITDA, book value coupled with other substantial benefits over competitors. Healthy growing stream of franchise income from Fuddruckers. Expanding Partnerships to share Luby's food in grocery stores such as the H-E-B 270 grocery locations, expanding franchise partnerships such as Fuddruckers and TravelCenters of America. 4 new franchised Fruddruckers already opened in 2017. Profitable Culinary Contract Services. Valuable real estate portfolio likely worth more than current enterprise value. Ability to initiate a sale lease back on close to 100 locations. Going private.

Additional information can be found in their January 25, 2017 investor presentation.

http://lubysinc.com/investors/events/files/Investor-Presentation-Q1-2017-01-25.pdf

Long LUB

IMN $.69 to be added during this week.