Note the stock has had a big run, ~ 100% since this post. Today 11/13/17 there has been heavy insider selling. I've sold my position.

Universal Technical Institute (UTI) offers postsecondary education careers for professional automotive, diesel, collision repair, motorcycle and marine technicians since 1965. It has 12 campuses across the United States. Additional offerings are individual electives, manufacturer/dealer sponsored training and MSAT (MANUFACTURER-SPECIFIC ADVANCED TRAINING).

12/20/16 profit taking by STADIUM CAPITAL PARTNERS L P. UTI has doubled since this post at $1.60, market close price 12/19/16 $3.30

Universal Technical Institute (UTI) offers postsecondary education careers for professional automotive, diesel, collision repair, motorcycle and marine technicians since 1965. It has 12 campuses across the United States. Additional offerings are individual electives, manufacturer/dealer sponsored training and MSAT (MANUFACTURER-SPECIFIC ADVANCED TRAINING).

12/20/16 profit taking by STADIUM CAPITAL PARTNERS L P. UTI has doubled since this post at $1.60, market close price 12/19/16 $3.30

News on 10/17/16: "NASCAR Technical Institute Partners with FCA US LLC to Offer Mopar Technical Education Curriculum Training Program"

Summary Investing Points:

-) High barriers to entry with +50 years focused experience, industry relationships, facilities are highly specialized with equipment, engines, truck, and cars on location makes creating duplication near insurmountable.

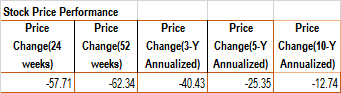

-) Deep historical and relative valuation discount. P/S and P/B at historical lows with potential mean reverting stock performance. 6.31 per share in TTM gross profit versus market price of $1.60 on post date 10/10/16, cash per share of $4.44, P/TB .29, P/S .11, stock price is 72% off 52 week high, 9% off 52 week low, UTI is 97% off P/B high, 3% off P/B Low ; 97% off P/S high, at historical low P/S

-) Convincing large drop in shorts as a % of float, largest drop in short as a % of float in the Education and Training Services industry. The average short % of float over the last 10 reported periods was 3. versus the current % of shares short at 1.24%.

-) Ignored by wall street with only one investor analyst on the 2016 earnings call.

-) Tarnished by the negative news in the for profit school industry without comparable negatives. "In fact, at the end of the third quarter, we had more than 7,200 jobs available in a quarter where we had approximately 1,700 graduates. As the need for skilled employees grow, and the call for the type of education that produces work-ready graduates gets louder, there is growing support for the kind of industry driven jobs focused programs we pioneered and continue to provide." Serious shortage of skilled auto mechanics looming, article from USA today. http://usat.ly/1Qb80Hc

-) 70 million capital raise from Coliseum capital (700,000 shares of convertible preferred stock announced on 06/24/16) for expansion via new geographic markets and leverage excess capacity for new skilled trade programs.

Note: Coliseum Capital Management owns 3,640,799 shares or 14% of total

shares outstanding as of 03/13/16. Then on 06/24/16 Coliseum purchased 700,000 convertible

preferred stock for a total value of $70,000,000. This

investment returns 7.5% annually with liquidation preference. “The Series a Preferred Stock may

be converted only to the extent that the number of shares of common stock

issued upon conversion does not exceed 4.99% of the total share of common stock

outstanding on the issue date (Conversion Cap). The Conversion Cap was

calculated to be 1,225,227 shares

on the issue date of June 24,

2016, and may be removed upon common stockholder approval.” Initial

conversion

price is $3.33 per share. Additionally I believe there were tax benefits

accrued to Coliseum as a 10% owner purchasing the preferred stock.

-) Restructuring and other cost savings announced on 09/26/16, reaffirmed 2016 fiscal year end outlook.Fiscal 2017 expense estimate saving of approximately 25 to 30 million.

-) Hidden off balance sheet assets of 118,194,000. This 118.194M balance represents the outstanding receivable for the proprietary loan program per the most recent 10q. Bank originates loans for students who meet specific credit criteria with the proceeds used to fund a portion of their tuition. UTI takes the most conservative accounting approach by not recognizing the receivable, interest accrued or its related revenue until the money is received. UTI committed to provide student loans for approximately $139.9 million since inception versus the current balance 118.194M.

Recognizing only 35% of the current receivable value is substantial. At .35(118.194) is 41.36M versus the current market value of 38.96M and enterprise value of -24.89M per Yahoo finance.

-) Real estate on the books below fair market value. UTI owns land/building of 95,000 square feet campus in Dallas Texas. Houston Texas Campus 172,000 square feet owned and lease the remaining 49,100.

It’s UTI 51 years of experience with strong industry leading OEM relationships

in the automotive, diesel, motorcycle, and marine industry creates UTI’s strong

moat. Potential competitor face near impossible conditions to duplicate. A competitive

challenger must locate in key USA cities to attract students. Then develop trusted

manufacturer relationships, purchase specific industry capital equipment,

develop the curriculum/course content using the vehicles, equipment,

and specialty tools to understand the requirements for qualified service

professionals. The industry oriented educational philosophy and national

presence have enabled industry relationships which provide a significant

competitive strength and supports UTI’s market leadership. UTI is often the

sole provider of MSAT with over 30 OEMs relationships.

Conclusion:

UTI is asset cheap and

oversold trading at a low valuation. Its financially sound with limited

downside, lower expense base after restructuring with operational leverage. Its

strong defendable moat has growing demand for their quality industry recognized

services.

Additional Supporting Tables

Current Valuation Measures from Yahoo Finance.